Subscribe to our newsletter

The place for unfiltered climate news and Deep Sky developments.

Uninsurable

Florida’s Home Insurance Collapse Signals National Trend

Executive Summary

Florida's home insurance market is in free fall. In just ten years, the total number of active home insurance policies has plummeted 78%, while the state's insurer of last resort has ballooned from 6% to 63% market share. Average premiums have increased 18% yet insurers continue their exodus.

This collapse isn't a temporary market adjustment. As Dave Jones, the former insurance commissioner of California put it: “The insurance crisis in the U.S. is the canary in the coal mine, and the canary is dead”. It’s the financial system's early warning of climate catastrophe. As hurricanes intensify and floods worsen, private insurers have concluded that large areas of real estate are essentially uninsurable at any price homeowners can afford. When the next major hurricane strikes, potentially affecting thousands of uninsured properties, the ripple effects will devastate Florida's real estate market and reverberate through financial markets nationwide.

Key Findings

- More uninsured Floridians: The number of home insurance policies is down 78% from over 3 million to 700,000 in just a decade

- Private market dwindling: Citizens Property Insurance Corporation now holds 63% market share, up from 6% in 2014

- Premiums at breaking point: Average annual premium reached $3,454 in 2024, up 22% since 2014

- Flooding costs jumping: National Flood Insurance Program payouts in 2024 were more than in the previous 14 years combined.

Introduction

Climate change is changing the math behind our insurance system, and, as top insurers like Allianz warn, poses a systemic risk to economic stability. Deep Sky Research found that wildfires are accelerating this trend in Western states like California, but Florida may be even closer to the cliff.

Florida sits at the intersection of multiple climate threats: intensifying hurricanes, rising sea levels, and increasing flood risk. Deep Sky Research's previous analysis found that the frequency of extreme hurricane rainfall has jumped 300% over the past four decades, with hurricanes that previously occurred once every 100 years now happening every 25. Maximum hurricane rainfall severity has grown 33%, lifting the ceiling on potential damage. These trends are forcing insurers to flee states like Florida.

Unlike gradual climate impacts that unfold over decades, insurance market disruption is happening rapidly. The data reveal not a temporary adjustment but a fundamental breakdown in the ability to price and distribute climate risk through traditional market mechanisms.

This report analyzes new data from the Florida Office of Insurance Regulation to map home insurance trends across the state. The analysis focuses on owner-occupied residential homeowners excluding tenants and condominiums.

The Great Insurance Retreat

Insurers Are Abandoning Florida Homeowners

The scale of the insurance exodus from Florida is unprecedented. Between 2014 and 2024, the total number of active home insurance policies across all Florida insurers collapsed from 3.2 million to just 710,000—a staggering 78% decline. There are fewer than a quarter of the policies today than there were 10 years ago.

Figure 1

In the last quarter of 2014, insurers wrote 164,000 new policies. By 2024, that number had plummeted to 37,000—a 77% collapse in new business.

Multiple major insurers have completely withdrawn from the state. Those remaining have dramatically restricted their exposure, refusing to write new policies in high-risk areas or implementing strict underwriting criteria that exclude most applicants. The message from the private market is clear: many Florida homes have become too risky to insure.

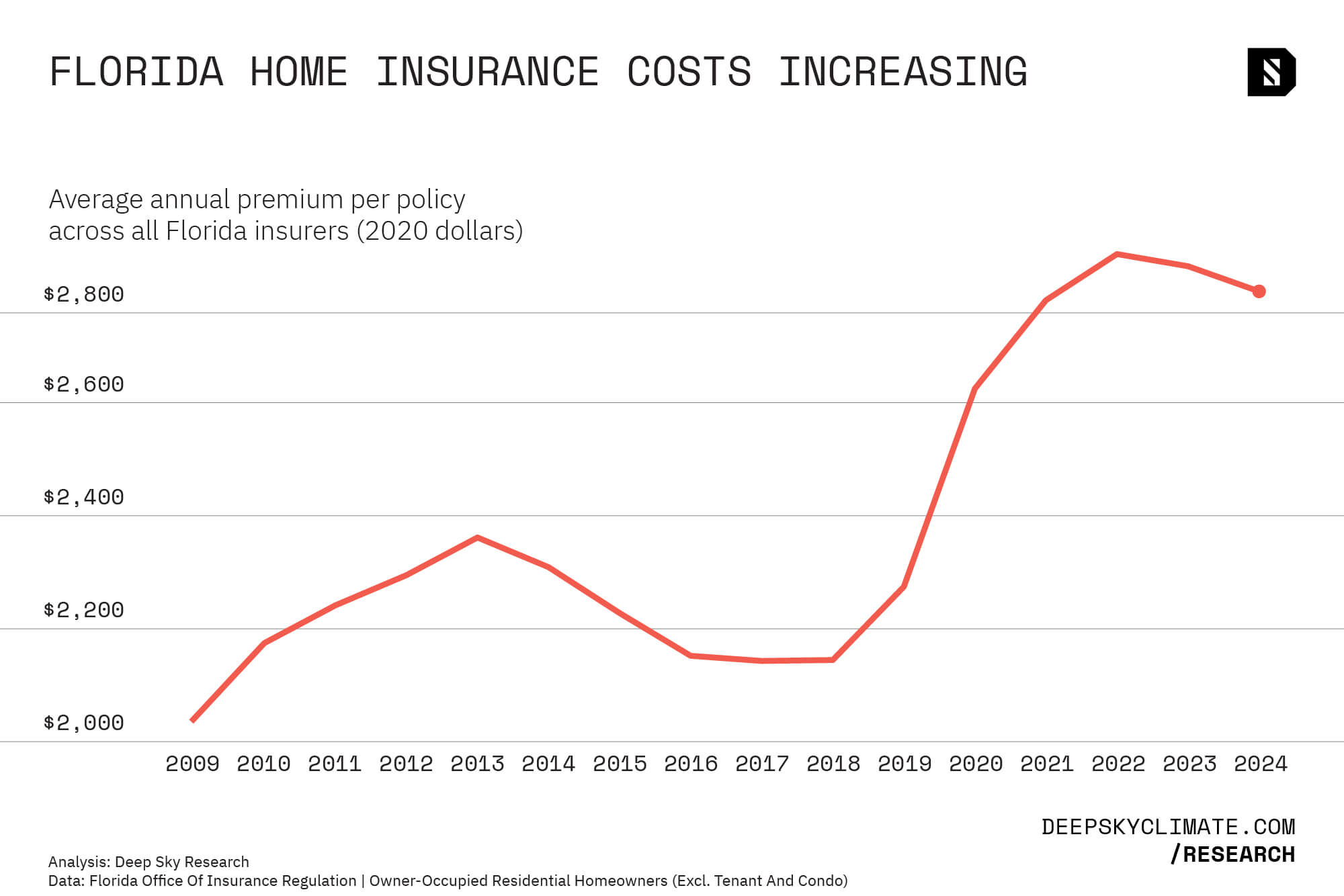

Premiums Climbing

Even as insurers leave, those remaining have dramatically increased prices. The average annual premium per policy across all Florida insurers has increased from $2,132 in 2014 to $3,454 in 2024. Accounting for inflation that amounts to a 22% cost increase. As cost of living has soared across the board, home insurance has outpaced other expenses and squeezed homeowners into a perilous situation.

Figure 2

These premium increases reflect insurers' attempts to price in escalating climate risk. Yet even at these elevated rates, insurers continue to lose money and exit the market, suggesting that actuarially sound pricing would push premiums far beyond what homeowners could afford.

The premium spiral creates a vicious feedback loop: as prices rise, more homeowners drop coverage or are forced onto the state plan, further concentrating risk and driving up costs for those who remain in the private market. Cost increases like this are particularly painful for homeowners when inflation is raising the cost of living across the board.

Citizens Property Insurance: From Safety Net to Market Dominant

The State Takes Over

As private insurers retreat, Citizens Property Insurance Corporation—Florida's insurer of last resort—has exploded from a minor market participant to the dominant force in Florida home insurance. In 2014, Citizens held just 6% of the market. By 2024, it commanded 63% market share, insuring the majority of Florida homes.

This transformation mirrors a similar trend to the one Deep Sky Research documented in California, where the FAIR plan more than doubled in size between 2020 and 2024. But Florida's situation is even more severe—Citizens now operates as the de facto primary insurer for most of the state.

Figure 3

Citizens was not designed to function at this scale. Created as a temporary backstop for homeowners unable to find private coverage, it lacks the capital reserves, risk management infrastructure, and geographic diversification of traditional insurers. Its dominance represents a market failure.

The Hidden Tax on All Floridians

Citizens' structure conceals a dangerous reality: when catastrophic losses exceed its reserves, every Florida insurance customer becomes liable for the shortfall—not just Citizens policyholders. Through what's called an assessment mechanism, Citizens can levy surcharges on all property and casualty insurance policies in the state, including auto, boat, pet, and renters insurance.

This means a renter in inland Tallahassee who has never owned property could see their auto insurance premiums spike to bail out Citizens after a major hurricane. A boat owner in Jacksonville faces higher premiums to cover losses from Miami beach homes. This socialization of climate risk across all Florida insurance customers represents a massive hidden tax that most residents don't understand until the bills arrive.

Senator Sheldon Whitehouse, who chairs the Senate Budget Committee and is investigating Citizens' viability, warned that "recouping billions of dollars in losses from Floridians is unlikely to be feasible economically or politically, let alone in time to pay massive claims." While Citizens maintains it has $15 billion in resources to handle claims, a truly catastrophic hurricane season could easily exceed this capacity, triggering widespread assessments that would further strain an already struggling population.

Even the Safety Net Becomes Unaffordable

Even Citizens' premiums have become unaffordable for many Floridians. The average annual premium for Citizens policies reached $3,348 in 2024, approaching private market rates. This defeats the entire purpose of an insurer of last resort—providing affordable coverage when the private market fails.

Citizens faces an impossible dilemma: charge actuarially sound rates that reflect true risk (making coverage unaffordable for most) or maintain subsidized rates that could bankrupt the program when the next major hurricane strikes. Neither option is sustainable.

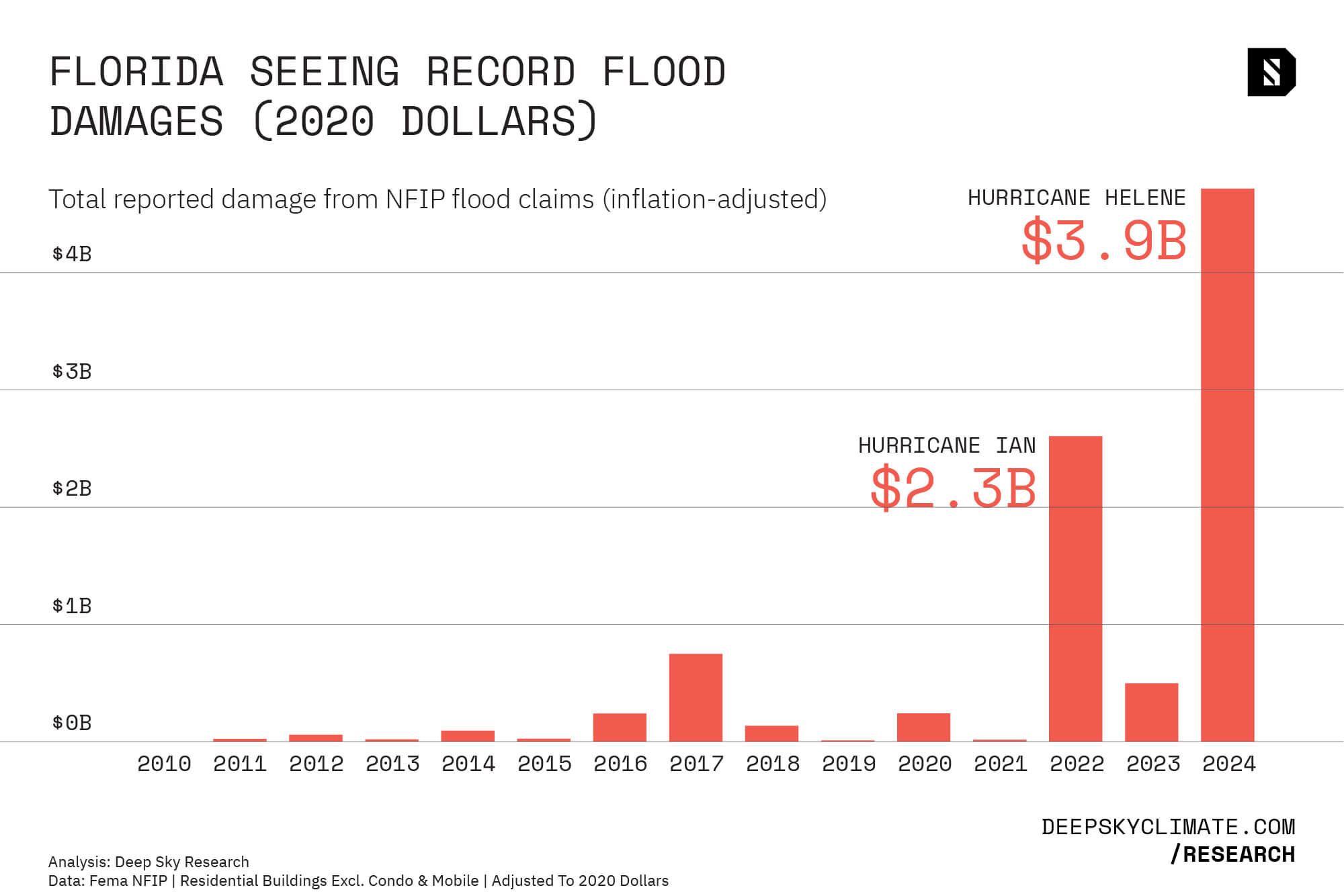

National Flood Insurance

Another component of the home insurance landscape in Florida is FEMA’s National Flood Insurance Program (NFIP). Homes located in FEMA designated regulatory floodplains are required to purchase flood-specific insurance in order to access a federally-backed mortgage.

Flooding damages are so costly that the private market was proving inadequate and the federal government had to step in. But this program is not immune to the risks plaguing other insurance programs.

Two of the last three years have seen enormous flooding damages, primarily due to Hurricanes Ian and Helene. NFIP outlays in these years have been enormous.

Figure 4

Climate Change: The Driving Force

It’s the Water

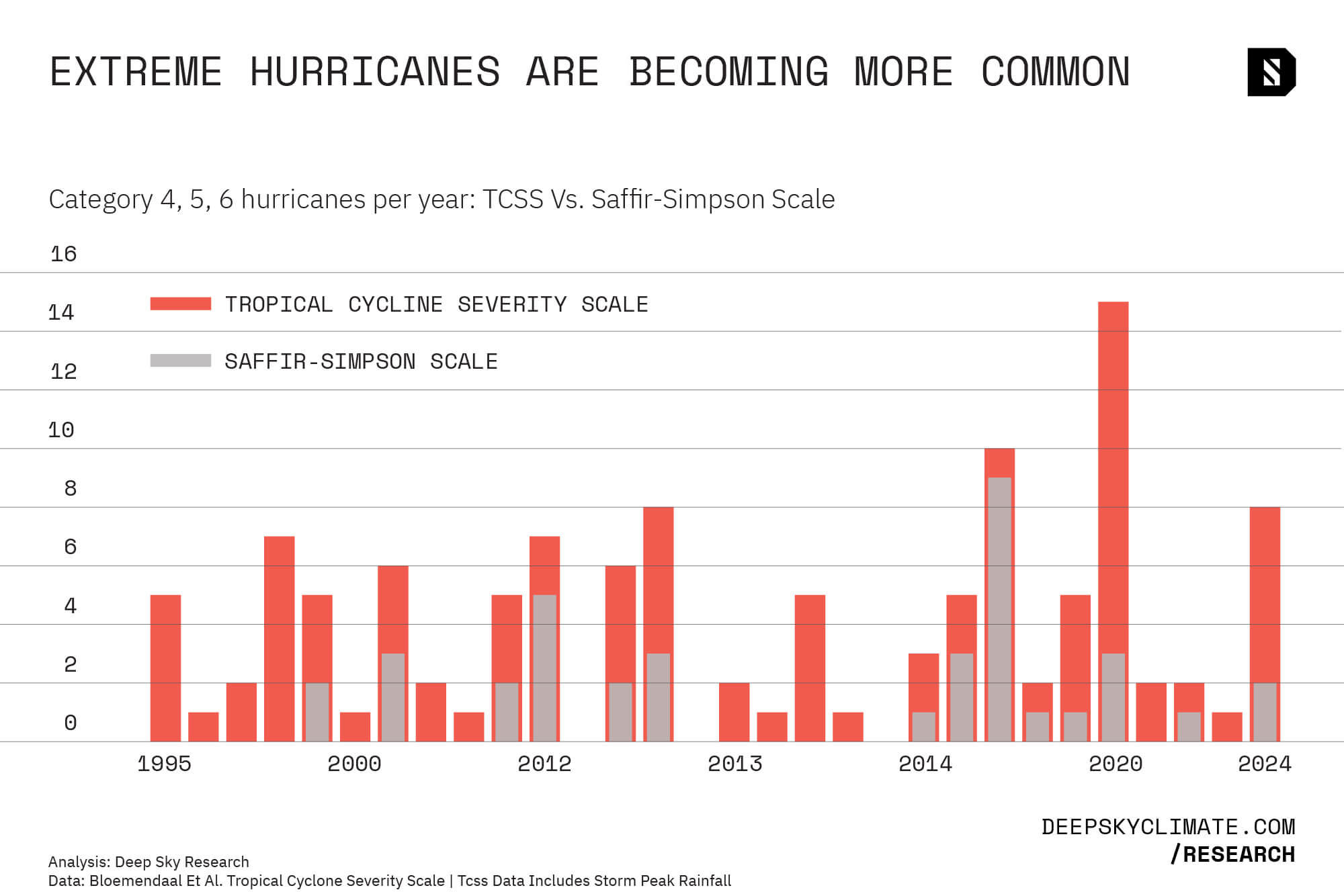

Hurricanes are usually discussed on the news in terms of their “category”. A Category 5 hurricane is extreme while a Category 2 storm may not raise your blood pressure. But this categorization system, called the Saffir-Simpson scale, is based on wind speed alone. The majority of hurricane damage is caused by water, not wind.

A new paper by Mol et al. (2025) advocates for a revamped system which considers not just wind speed but also rainfall and storm surge – rapid seawater level rise caused by tropical storms. The Tropical Cyclone Severity Scale (TCSS) measures hurricanes on a more complete set of metrics and can also improve our understanding of trends in hurricane severity.

Compound Threats

- Extreme windspeeds: Hurricane wind can cause significant property damage, but it is far from the only risk factor.

- Storm surge: Rising sea levels mean hurricane storm surges penetrate further inland and cause more severe flooding.

- Torrential rainfall: Maximum hurricane rainfall amounts have increased by 33%, which spread destruction to inland areas unprepared for hurricanes.

Figure 5

Deep Sky Research analyzed data provided by the author of the paper, Dr. Bloemendaal. When considering all three destructive components of hurricanes to categorize storms, it is clear that the frequency of extreme hurricanes (Category 4, 5, or 6) is increasing. 2020 was a record-breaking year and 2024 ranked tied 3rd highest since 1995.

This trend is not immediately obvious from the Saffir-Simpson scale. Climate scientists debate climate change’s impact on hurricanes’ extreme winds, but it is well established that a warmer atmosphere holds more moisture and thereby causes more extreme rainfall. Similarly, warmer oceans cause sea level rise and contribute to larger, more dangerous storm surge.

Figure 6

The TCSS scale does a better job of tracking hurricane destruction, which is why it aligns with home insurers’ actions. Largely via increased flood risk, hurricanes are becoming more common and more extreme.

Market Breakdown Accelerates

The Death Spiral

Florida's insurance market has entered what economists call a "death spiral"—a self-reinforcing cycle of market collapse:

- Climate risks increase, driving up insurer losses

- Insurers raise premiums or exit the market entirely

- Healthy homeowners drop coverage or move to Citizens

- Risk concentrates among remaining private insurers

- Losses mount, forcing more exits and price increases

- The cycle accelerates

This spiral is evident in the 77% collapse in new policies written. Without new customers to spread risk, the insurance pool becomes increasingly concentrated among the highest-risk properties that have no alternatives.

Geographic Risk Concentration

Unlike national insurers that can diversify across regions, Citizens concentrates 100% of its risk in the most hurricane-vulnerable state in America. A single major hurricane could overwhelm its reserves, triggering assessments on all Florida property insurance policies—including auto and business coverage—to cover shortfalls.

This concentration makes Citizens essentially a massive uncovered bet against climate change. When that bet inevitably fails, Florida taxpayers and policyholders will bear the losses.

Broader Economic Implications

Real Estate Market Impacts

The insurance crisis threatens to trigger a Florida real estate collapse. Banks require insurance for mortgages; without affordable coverage, property transactions freeze. Cash buyers might purchase uninsured homes at steep discounts, but this would crater property values across the state.

Florida's economy depends heavily on real estate, construction, and tourism—all vulnerable to an insurance-driven property crisis. A significant drop in home values would devastate household wealth, reduce property tax revenues, and trigger a recession.

Financial Contagion Risk

Florida's insurance collapse won't remain contained. National banks hold hundreds of billions in Florida mortgages that could become distressed if properties become uninsurable. Real estate investment trusts (REITs) with Florida exposure would see valuations plummet. Municipal bonds backed by property taxes could face downgrades or defaults.

As Deep Sky Research noted regarding California's wildfire insurance crisis: "Insurance markets are a leading indicator of how financial markets will deal with the climate crisis. Just as insurers won't do business in key areas now, so too will investors avoid those kinds of risks."

Conclusion

Insurance markets are pricing in climate reality while politics and policy lag behind. Florida’s home insurance market warning signs from an economic system beginning to buckle under climate pressure.

The question is no longer whether Florida's insurance market will stabilize—it won't under current climate trajectories. The question is whether policymakers will acknowledge this reality and implement transformative adaptation measures, or whether market forces will impose their own solutions through property abandonment, displacement, and huge losses.

Time is running out. The 2025 hurricane season has been relatively quiet so far, but if 2024 was any indication, it could ramp up anytime. Just one big storm this fall brings potential for catastrophic losses to thousands of uninsured Florida homes. The insurance market has delivered its verdict on climate risk and the rest of the economy will soon follow.

About Deep Sky Research

Deep Sky Research provides cutting-edge climate risk analysis and research, combining advanced data analytics with deep expertise in climate science and financial markets. Our reports inform investors, policymakers, and the public about the accelerating impacts of climate change on economic systems.

Data Sources

Analysis based on data from the Florida Office of Insurance Regulation tracking owner-occupied residential homeowners insurance (excluding tenant and condo policies) from 2009-2024. Premium and policy data covers all admitted insurers operating in Florida. Citizens Property Insurance Corporation data analyzed separately as the state's insurer of last resort.

- https://www.linkedin.com/pulse/climate-risk-insurance-future-capitalism-g%C3%BCnther-thallinger-smw5f/

- https://www.deepskyclimate.com/blog/insurers-retreat-as-2025-wildfire-risk-reaches-dangerous-levels

- Deep Sky Research, "Frequency of Deadly Hurricane Weather has Jumped 300%," 2024. Available at: https://www.deepskyclimate.com/blog/frequency-of-deadly-hurricane-weather-has-jumped-300

- https://www.deepskyclimate.com/blog/insurers-retreat-as-2025-wildfire-risk-reaches-dangerous-levels

- "Florida's home insurer of last resort is in serious trouble. Will Milton put it over the edge?" CNN Business, October 11, 2024. Available at: https://www.cnn.com/2024/10/11/business/citizens-insurance-hurricane-milton

- Mol, J.M., Bloemendaal, N., de Moel, H. et al. An experimental test of risk perceptions under a new hurricane classification system. Sci Rep 15, 30320 (2025). https://doi.org/10.1038/s41598-025-14170-1

- Bloemendaal, Nadia; de Moel, Hans; Mol, Jantsje M.; Bosma, Priscilla R.M.; Polen, Amy; and Collins, Jennifer M., "Adequately Reflecting the Severity of Tropical Cyclones Using the New Tropical Cyclone Severity Scale" (2021). School of Geosciences Faculty and Staff Publications. 2307.